As more and more companies embed AI into select functions, only a portion indicate that they have used AI to change how an overall enterprise runs.

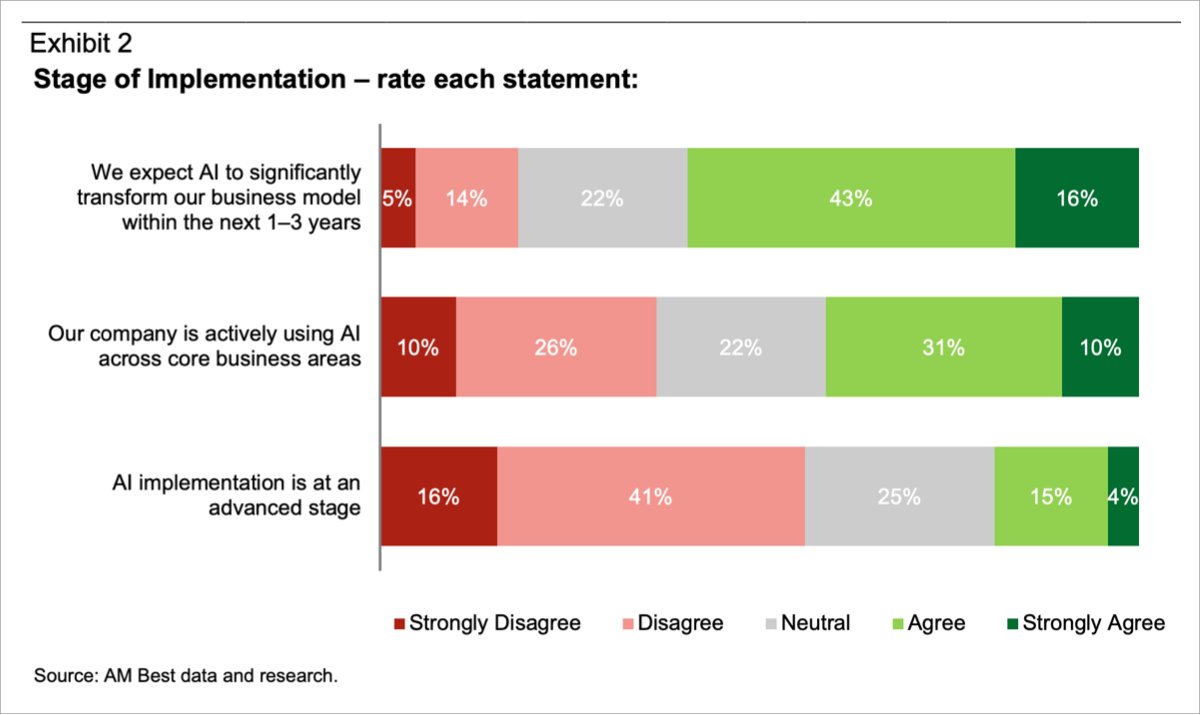

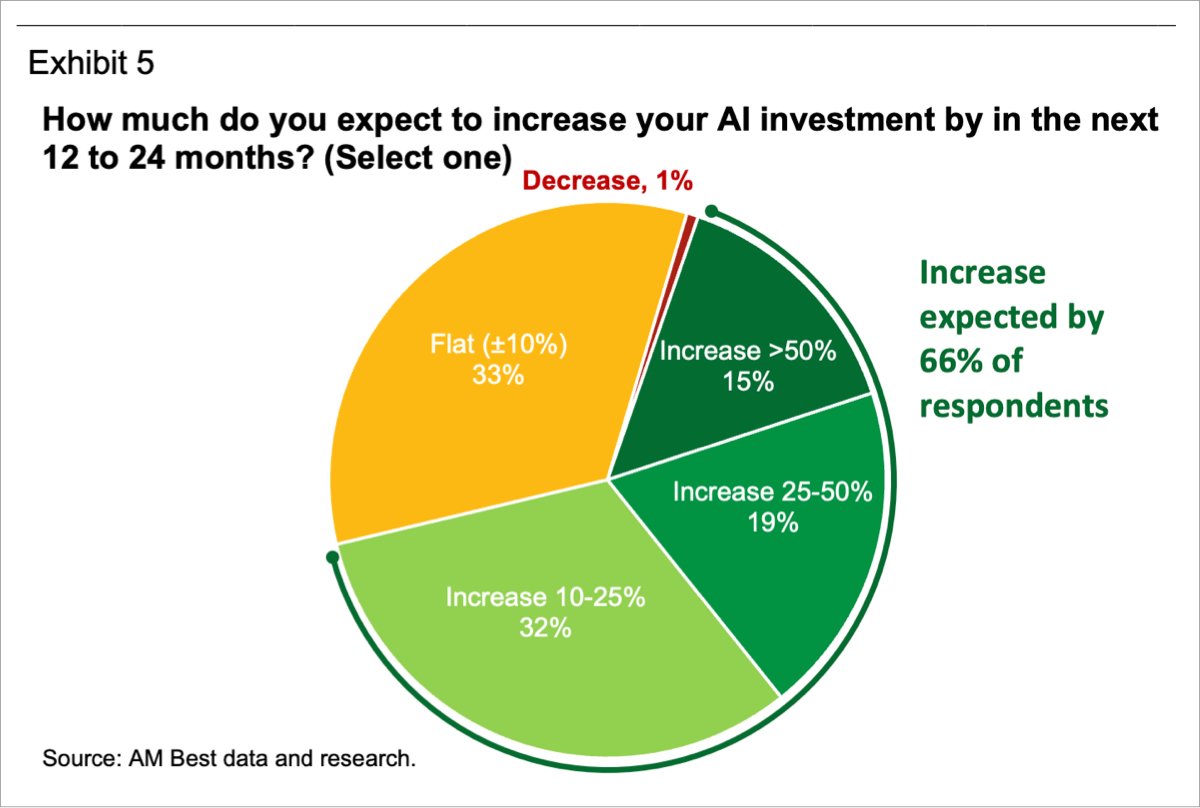

It illustrates one of the key takeaways drawn from a recent industry survey by AM Best on AI use – measuring the gap between basic, preliminary adoption and measuring transformational outcomes. Nearly 60% of respondents expect AI to significantly transform their business model within the next one to three years.

But approximately just one in five say that their AI implementation is already at an advanced stage. Approximately 150 rated carriers and managing general agents responded to the survey questions posed in November 2025. Results show that companies are increasing their investment in AI to boost productivity, streamline processes, and gain competitive advantage amongst their peers. Unsurprisingly, insurers have identified themselves as risk averse and less advanced than other industries in technology.

The ambition is clearly there, but the realized value is still uneven. In other words, the technology may be maturing faster than the operating models around it. This execution reality was reflected in the survey as 53% of respondents described themselves as cautious pacesetters rather than first movers.

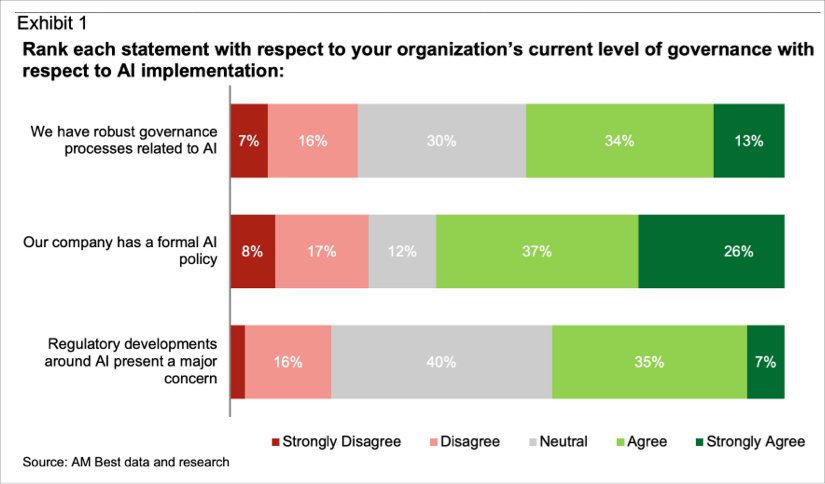

This approach makes sense for a regulated and legacy-heavy industry with a fiduciary duty to its policyholders. Scaling AI here requires more than just the tools. It requires data readiness, workflow redesign, governance, privacy and security controls, vendor oversight, and clear accountability for how AI-supported decisions are made.

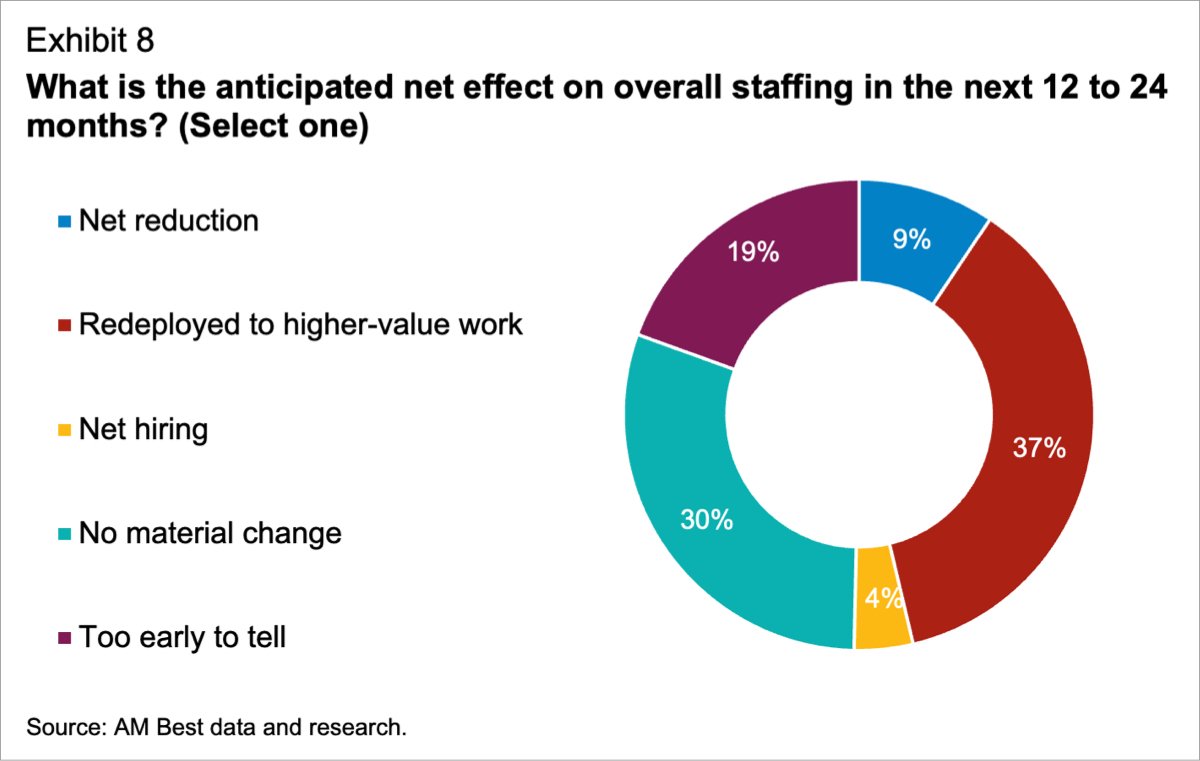

(Editor’s note: The survey-based graphics in this article are sourced from AM Best’s report titled “Artificial Intelligence Appears to Be Ready, But Most Insurers Are Not,” which was published on April 27.)

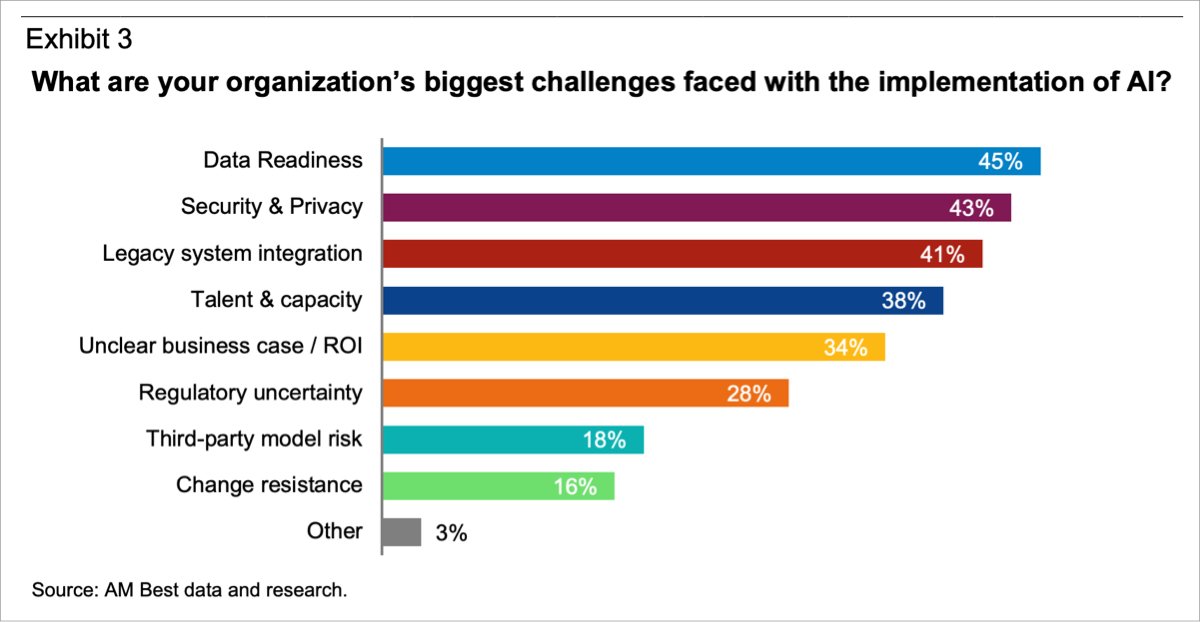

Friction remains for insurers with survey respondents indicating that the top challenges are data readiness (45%), security and privacy (43%), and legacy system integration (41%). (See Exhibit 3). Those shouldn’t necessarily be viewed as three separate and individual problems. These should be considered different manifestations, if of the same underlying issue, which is whether the enterprise data and system environment is mature enough to support AI safely and at scale.

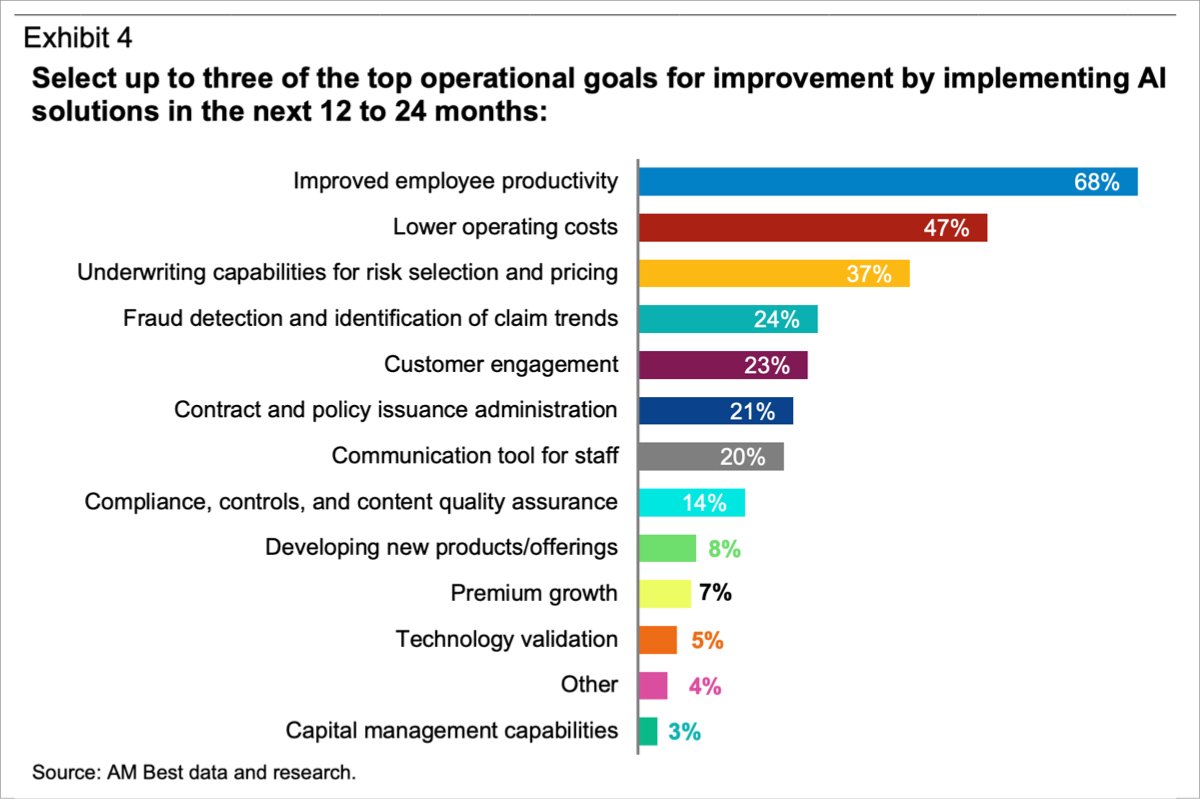

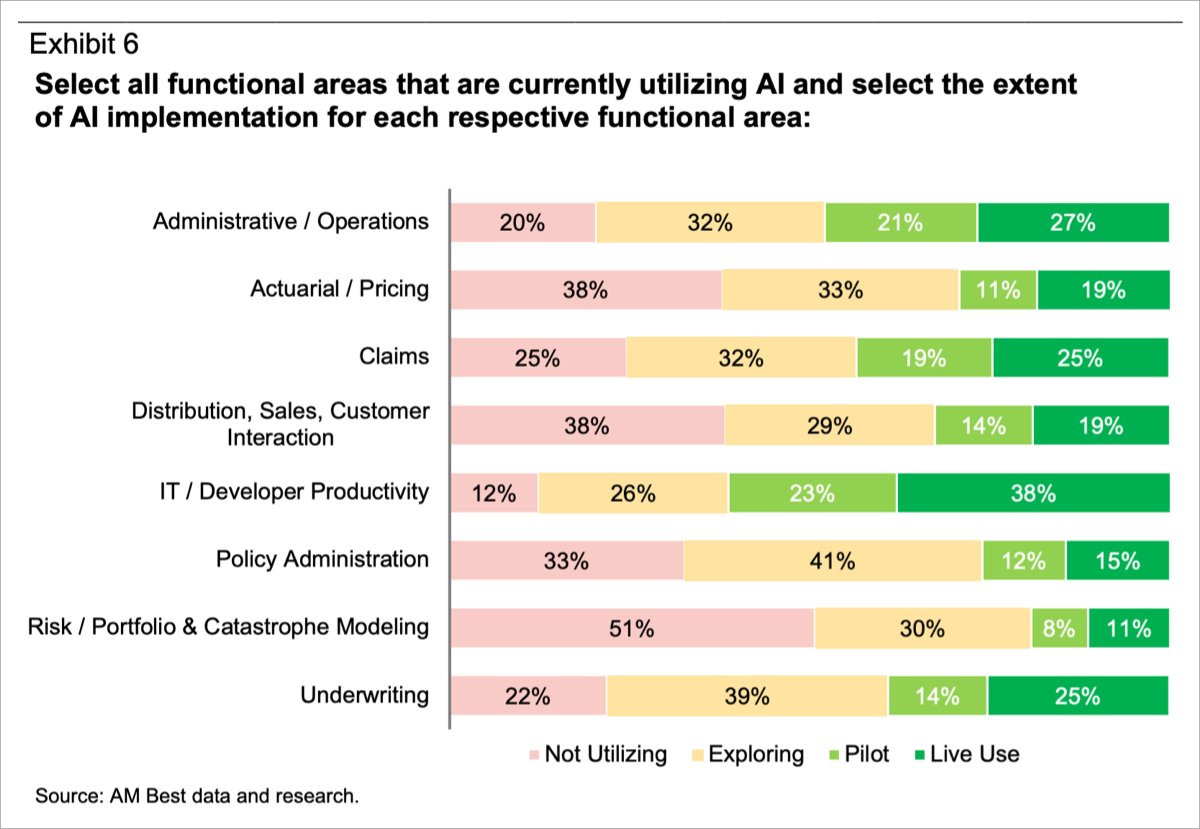

According to survey respondents, live use of AI is most evident in areas such as IT/developer productivity, administrative operations, underwriting, and claims. AI tools have really helped enable insurers to automate many administrative and operational tasks, such as data entry and document manipulation.

AI tools, including machine learning and potentially more agentic systems as they mature, can support underwriting by analyzing large data sets and helping segment submissions by risk characteristics. Lower-complexity risks may be automated or triaged for lighter review, while underwriters can focus more attention on complex cases requiring judgment.

Insurance companies have enormous amounts of data, but that is often spread across older systems and fragmented workflows. AI can generate a lot of value from that data, but only if it is clean, connected, well-governed, and perhaps more importantly — usable.

Perhaps a more cautionary note, only 18% of respondents considered third-party model risk as a challenge. That’s a bit challenging to square with 68% of respondents indicating that third-party solutions are one of the sources of their AI development.

In a regulated industry where insurers remain accountable for the AI that that their vendors deploy, one might have expected that risk to sit a little bit higher. Our expectation is that this issue may move higher on risk radars as adoption matures and as supervisory focus on vendor oversight continues to increase.

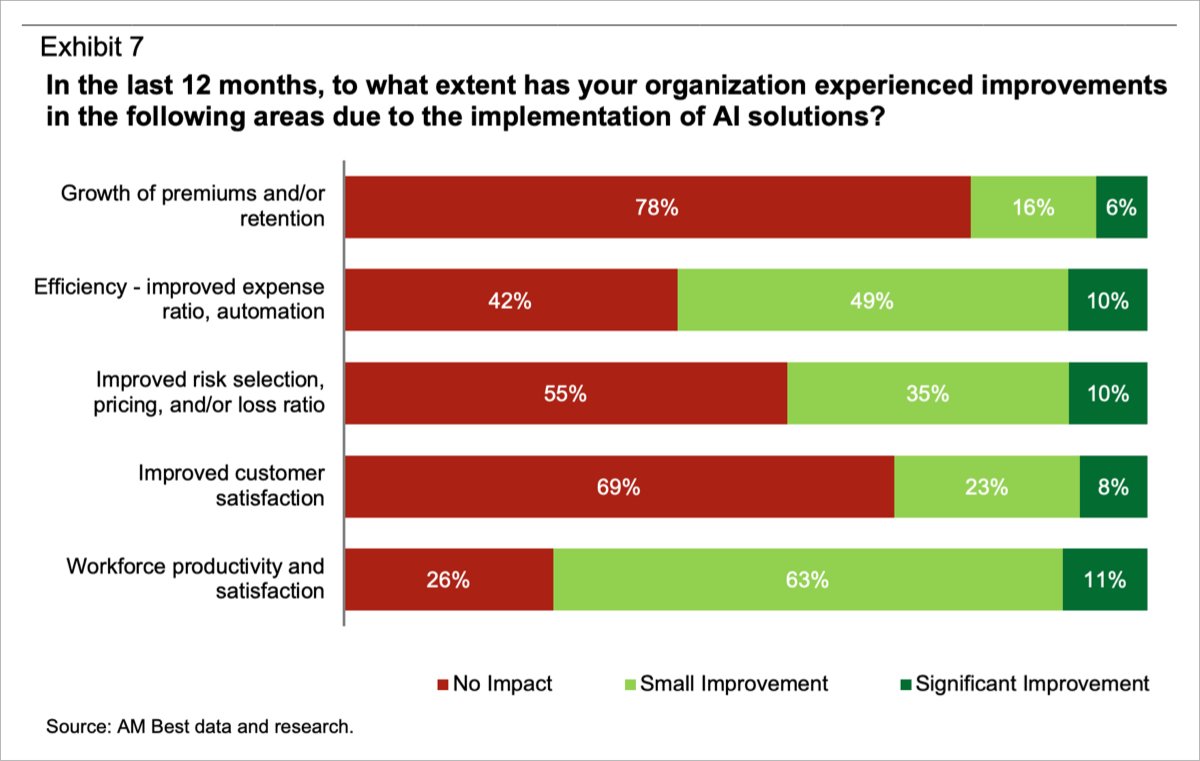

A return on investment can be difficult to measure at the early stages of implementation. Some of the technology being utilized is still relatively new and cost benefits will likely take years to materialize. Only 13% of survey respondents felt very confident in their organization’s ability to accurately develop an AI ROI measurement.

What we’re seeing though is improvement in workforce productivity and satisfaction has seen the biggest impact with 63% of respondents reporting a small improvement in addition to another 11% reporting a significant improvement. There’s also been a prominent improvement in efficiency regarding improved expense ratio and automation as 49% of respondents noted a small improvement and 10% noted a significant improvement.

For insurers, AI readiness is not a one-time milestone. It is a moving target that will require governance, data infrastructure, workforce capabilities, and risk controls that can evolve as quickly as the technology itself.

Topics InsurTech Data Driven Artificial Intelligence Carriers

Interested in Ai?

Get automatic alerts for this topic.

Source link