Investing 500 euros per month means laying a solid foundation for building your assets. But a question arises: how to invest 500 euros per month intelligently ?

Invest in the stock market, in real estate, open the best stock savings plan (PEA)the best life insurancethe best retirement savings plan (PER)…the options are numerous, and you can quickly get lost.

💡 Before investing 500 euros per month, we must ask yourself the right questions : what is my investment horizon? What level of risk do I accept? What distribution between the different asset classes (shares, bonds, real estate)?

➡️ In reality, investing 500 euros per month can become a powerful lever for building significant wealth… provided you structure your strategy correctly from the start.

In the long term, thanks to compound interest, this effort can generate several hundred thousand, even millions of euros. But one thing is certain, it’s not just the amount that makes the difference. It is also regularity, yield, optimization of costs and the investment horizon.

📌 Here’s what you need to know before investing 500 euros per month:

- Before starting to invest €500 per month with your first savings, it is recommended to build up precautionary savings on best risk-free investments.

- Then we can start to invest for the long term. For this, it is possible toinvest in the stock market via trackers (ETF) within a PEA and/or a life insurance (which also gives access to best euro funds to secure part of the capital).

- Also, open a PER (among the best PER of the market) can be interesting if you have a marginal tax bracket (TMI) of 30% or more. The amount paid is deducted from our taxable income, which allows you to “put your income tax to work” for your retirement.

- To invest in real estate with part of these €500 per month: stone-paper constitutes a simple alternative, particularly via the real estate investment companies (SCPI).

- Adopt a long-term vision (10 years minimum) : it is essential to smooth out crises and benefit from market growth

💡 Notes d’Hugo : When you start, you tend to look for “the best investment” for your 500 euros per month. But the real subject is the overall strategy: choosing the right envelope (life insurance, PEA, PER, CTO), and the right allocation within the chosen envelopes (between stocks, bonds, real estate, etc.). And finally, like in sport, it’s not the perfect exercise that produces the result, it’s consistency. Those who succeed are not necessarily the most brilliant, but the most disciplined.

SUMMARY :

Invest 500 euros per month intelligently: simple 3-step method

📈 Investing 500 euros per month is not complicated, but you still have to do things in the right order.

Performance does not come from a miracle investment, but from a clear method: asset allocation → investment envelope → intermediary.

This is exactly what makes the difference between a saver who is fumbling… and a saver who is really building his wealth.

💡 We can see it like real estate construction: we start with the structure, then we choose the framework, and finally we refine the details. In investing, it all starts with distributing your money, even before choosing where to put it.

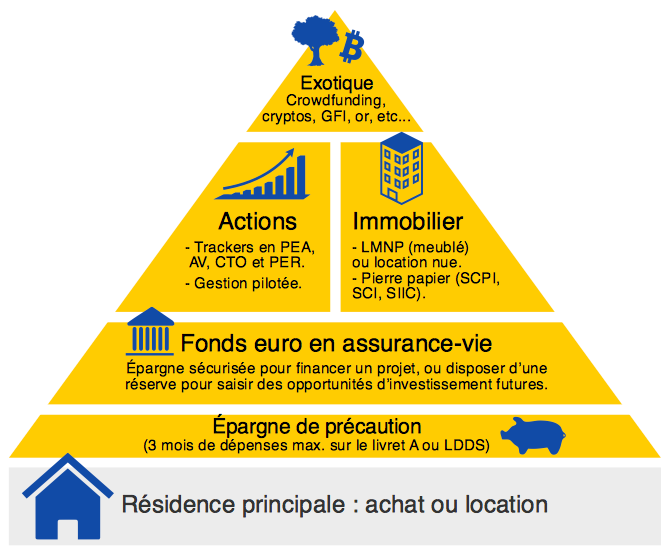

Step 1: define your allocation to invest 500 euros per month

Before talking about PEA or life insurance, we must answer a simple question: how to distribute your €500 each month? In other words, define your asset allocation.

➡️ The wealth pyramid is a good guide to knowing where to invest your €500 and in what order:

👉 We can reason simply by structuring our asset allocation as follows:

- actions to grow capital (e.g. via ETF shares in a PEA);

- secure investments to stabilize (e.g. via a euro funds in life insurance) ;

- possibly real estate to complete and diversify by taking advantage of credit leverage (e.g. via SCPI in life insurance) ;

- regarding the “exotic” category, it is clearly not obligatory, but may be relevant for significant assets to further diversify into non-financial assets (invest in gold, invest in cryptosetc.).

💡 Above all, before even defining your allocation, you must take the time to define your investor profile (risk profile) and its investment horizon. These are the two essential parameters that will guide our strategy.

Notes d’Hugo : a good asset allocationit’s the one that we understand and that we are able to maintain even when the markets fall. The real danger is not the fall in the markets, it is not supporting it and selling at the worst time. Here is our free Excel file to track your asset allocation.

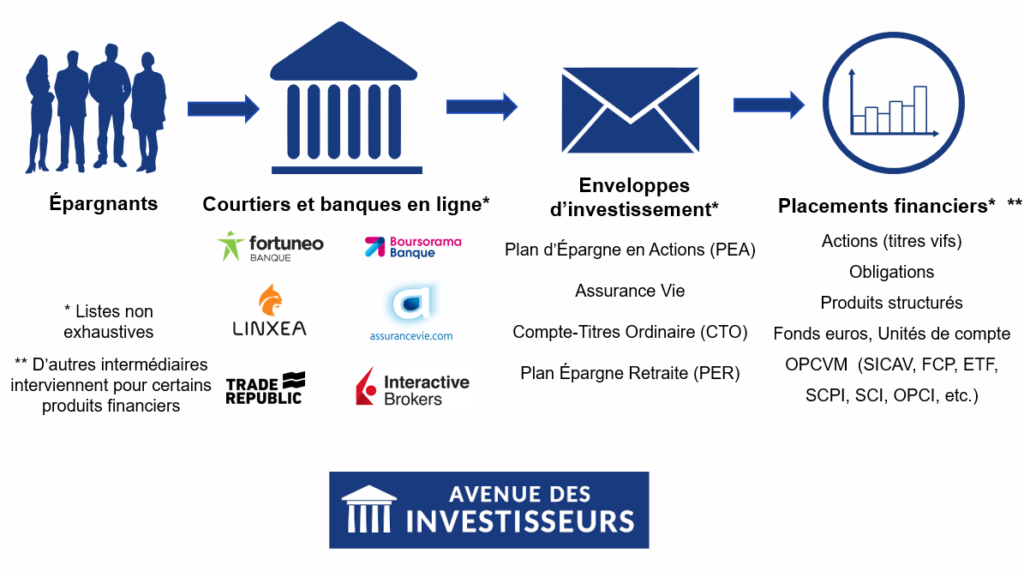

Step 2: choose the appropriate envelope to invest €500 per month

💡 Once the allocation has been defined, we choose the right tax framework. The envelope (PEA, life insurance, CTO, etc.) does not create performance in itself, but it allows it to be optimized by improving the net return after tax.

➡️ Here is a summary table of the specificities of the main envelopes:

💡 This table allows you to quickly understand what each envelope is used for according to its objective:

The key idea: each envelope has a specific role, and combining them intelligently allows you to optimize your strategy.

Notes d’Hugo : as Morgan Housel points out in his book “The Psychology of Money”, the best financial decision is not necessarily the most optimized on paper. An investor who wants to simplify his life and automate everything can choose to centralize everything (euro funds + equity ETF + real estate + gold) in good life insurance (the best life insurance). Result: rebalancing between investments is simple and you have the possibility of automating everything via scheduled payments. Investing well is not about seeking perfection, it is about finding a strategy that suits you and that you can stick with over time.

Step 3: choose the right intermediary

Last step, often neglected: the choice of the intermediary (the broker / bank with whom we open our PEA, our life insurance, etc.).

And it’s a good time to talk about the No. 1 enemy of all our investments: fees.

➡️ Here is a graph which allows us to see the impact of fees on our investments:

The choice of intermediary seems secondary at the start… but it is a major lever of performance over time.

👉 Two simple rules to remember:

💡 Fees are not the only criterion for selecting an intermediary to invest, there is also the quality of customer service, the funds available, the interface, etc. Our comparisons take this into account:

Investing 500 euros per month in the stock market: concrete example

Let’s move from theoretical to concrete. You want to invest €500 per month in the stock market because you already have precautionary savings (€5,000 in Livret A for example) and a long-term investment horizon.

Investing 500 euros per month in the stock market becomes simple as soon as you apply a clear method with a real profile in mind.

🔎 Let’s take an example: Julien, 38 years old, executive, 2 children, saves €500 per month. He has precautionary savings and a long-term horizon (10 years +). He accepts volatility (increases/decreases in his portfolio), but does not want to spend his evenings managing his portfolio.

Objective: to grow your capital without complexity, with a minimum of management time.

Example of a simple and robust allowance for €500/month

In this case, the most effective solution often remains the simplest. An allocation based on diversified ETFs allows you to obtain an excellent return/risk/simplicity ratio.

👉 Allocation chosen by Julien:

💡 Why this choice? The World ETF allows you to invest in more than 1,300 global companies in a single line. And the secure portion in euro funds makes it possible to cushion declines and to have “ammunition” aside to invest more heavily in ETFs in the event of a sharp decline in the stock markets.

👉 As for envelopes and intermediaries, Julien chooses:

Result: a simple strategy adapted to your profile.

Notes d’Hugo : In Julien’s case (and for many investors), simplicity is important. In practice, we see a lot of “new passionate investors” who want to test everything. But a few years later, a strategy that is too complex often ends up being counterproductive and abandoned. Ideally, our “us” in 10 or 20 years should still be able to follow and invest while respecting the allocation planned 10 or 20 years earlier.

💡 We tend to complicate investing… even though the basics are actually quite simple. Investing 500 euros per month effectively is based on a clear method, not on finding the perfect investment.

If we had to summarize:

- Define an allocation adapted to your risk profile and investment horizon.

- Choose the right envelopes (PEA, life insurance, CTO, PER).

- Select inexpensive and efficient online intermediaries (avoid traditional banks).

- Invest regularly, without being disturbed by the markets.

In other words: a simple, coherent and above all sustainable strategy over time.

➡️ In practice, for the majority of savers, this involves:

- Opening at least one life insurance policy and a quality PEA to “set a date” (i.e. start the tax seniority now, even with a small amount, to benefit later from the tax advantages of these envelopes) ;

- for the long term, invest regularly in one or more diversified ETFs, with potentially the use of a Lombard credit to generate cash flow and leverage;

- automate your investments when possible, to avoid emotional bias (automate life insurance payments).

📌 And for those who are heavily taxed (TMI ≥ 30%), the retirement savings plan (PER) can intelligently complement the strategy, in particular to benefit from the tax deduction (for example via the PER Lucya Cardif : see our review Lucya Cardif PER).

Invest €500 per month in delegating?

Need support and structure a tailor-made strategy?

If you already have significant assets (from €100,000), it may be relevant to get support. An advisor Prosper Conseil helps you implement advanced strategies with true capital and remuneration independence.

💡 Unlike traditional bankers and CGPs, Prosper Conseil advisors are paid solely by your fees (without commissions paid by partners) and have a completely open architecture (MiFID II regulations). Result: advice aligned with your interests, not with investments to sell.

➡️ Make an appointment with a Prosper Conseil advisor

➡️ If you prefer to become independent: read our site carefully, and/or our best seller book.

Source link